Page 59 - Accounting Information Systems

P. 59

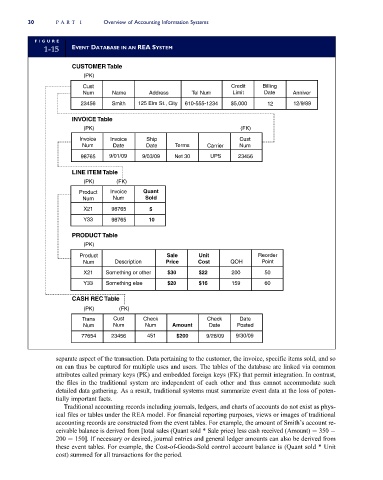

30 PART I Overview of Accounting Information Systems

FI G U RE

1-15 EVENT DATABASE IN AN REA SYSTEM

CUSTOMER Table

(PK)

Cust Credit Billing

Num Name Address Tel Num Limit Date Anniver

23456 Smith 125 Elm St., City 610-555-1234 $5,000 12 12/9/89

INVOICE Table

(PK) (FK)

Invoice Invoice Ship Cust

Num Date Date Terms Carrier Num

98765 9/01/09 9/03/09 Net 30 UPS 23456

LINE ITEM Table

(PK) (FK)

Product Invoice Quant

Num Num Sold

X21 98765 5

Y33 98765 10

PRODUCT Table

(PK)

Product Sale Unit Reorder

Num Description Price Cost QOH Point

X21 Something or other $30 $22 200 50

Y33 Something else $20 $16 159 60

CASH REC Table

(PK) (FK)

Trans Cust Check Check Date

Num Num Num Amount Date Posted

77654 23456 451 $200 9/28/09 9/30/09

separate aspect of the transaction. Data pertaining to the customer, the invoice, specific items sold, and so

on can thus be captured for multiple uses and users. The tables of the database are linked via common

attributes called primary keys (PK) and embedded foreign keys (FK) that permit integration. In contrast,

the files in the traditional system are independent of each other and thus cannot accommodate such

detailed data gathering. As a result, traditional systems must summarize event data at the loss of poten-

tially important facts.

Traditional accounting records including journals, ledgers, and charts of accounts do not exist as phys-

ical files or tables under the REA model. For financial reporting purposes, views or images of traditional

accounting records are constructed from the event tables. For example, the amount of Smith’s account re-

ceivable balance is derived from [total sales (Quant sold * Sale price) less cash received (Amount) ¼ 350

200 ¼ 150]. If necessary or desired, journal entries and general ledger amounts can also be derived from

these event tables. For example, the Cost-of-Goods-Sold control account balance is (Quant sold * Unit

cost) summed for all transactions for the period.