Page 569 -

P. 569

568 Part Four Building and Managing Systems

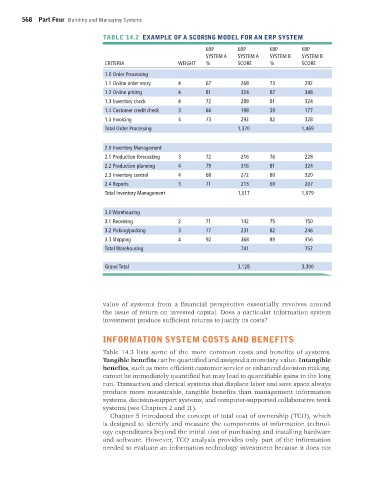

TABLE 14.2 EXAMPLE OF A SCORING MODEL FOR AN ERP SYSTEM

ERP ERP ERP ERP

SYSTEM A SYSTEM A SYSTEM B SYSTEM B

CRITERIA WEIGHT % SCORE % SCORE

1.0 Order Processing

1.1 Online order entry 4 67 268 73 292

1.2 Online pricing 4 81 324 87 348

1.3 Inventory check 4 72 288 81 324

1.4 Customer credit check 3 66 198 59 177

1.5 Invoicing 4 73 292 82 328

Total Order Processing 1,370 1,469

2.0 Inventory Management

2.1 Production forecasting 3 72 216 76 228

2.2 Production planning 4 79 316 81 324

2.3 Inventory control 4 68 272 80 320

2.4 Reports 3 71 213 69 207

Total Inventory Management 1,017 1,079

3.0 Warehousing

3.1 Receiving 2 71 142 75 150

3.2 Picking/packing 3 77 231 82 246

3.3 Shipping 4 92 368 89 356

Total Warehousing 741 752

Grand Total 3,128 3,300

value of systems from a financial perspective essentially revolves around

the issue of return on invested capital. Does a particular information system

investment produce sufficient returns to justify its costs?

INFORMATION SYSTEM COSTS AND BENEFITS

Table 14.3 lists some of the more common costs and benefits of systems.

Tangible benefits can be quantified and assigned a monetary value. Intangible

benefits, such as more efficient customer service or enhanced decision making,

cannot be immediately quantified but may lead to quantifiable gains in the long

run. Transaction and clerical systems that displace labor and save space always

produce more measurable, tangible benefits than management information

systems, decision-support systems, and computer- supported collaborative work

systems (see Chapters 2 and 11).

Chapter 5 introduced the concept of total cost of ownership (TCO), which

is designed to identify and measure the components of information technol-

ogy expenditures beyond the initial cost of purchasing and installing hardware

and software. However, TCO analysis provides only part of the information

needed to evaluate an information technology investment because it does not

MIS_13_Ch_14_global.indd 568 1/17/2013 2:31:59 PM