Page 170 -

P. 170

136 PART 2 • STRATEGY FORMULATION

evaluate strategies on items other than financial measures. This is the basic tenet of the

Balanced Scorecard. Financial measures and ratios are vitally important. However, of

equal importance are factors such as customer service, employee morale, product quality,

pollution abatement, business ethics, social responsibility, community involvement, and

other such items. In conjunction with financial measures, these “softer” factors comprise

an integral part of both the objective-setting process and the strategy-evaluation process.

These factors can vary by organization, but such items, along with financial measures,

comprise the essence of a Balanced Scorecard. A Balanced Scorecard for a firm is simply

a listing of all key objectives to work toward, along with an associated time dimension of

when each objective is to be accomplished, as well as a primary responsibility or contact

person, department, or division for each objective.

Types of Strategies

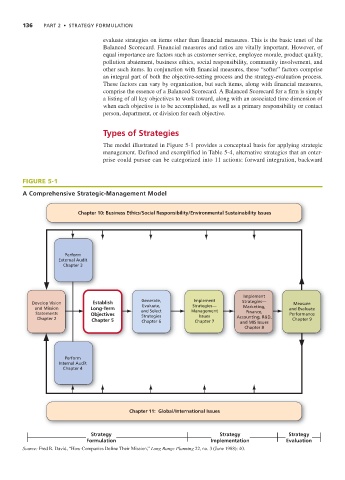

The model illustrated in Figure 5-1 provides a conceptual basis for applying strategic

management. Defined and exemplified in Table 5-4, alternative strategies that an enter-

prise could pursue can be categorized into 11 actions: forward integration, backward

FIGURE 5-1

A Comprehensive Strategic-Management Model

Chapter 10: Business Ethics/Social Responsibility/Environmental Sustainability Issues

Perform

External Audit

Chapter 3

Implement

Implement

Develop Vision Establish Generate, Strategies— Strategies— Measure

Evaluate,

and Mission Long-Term Marketing, and Evaluate

Statements Objectives and Select Management Finance, Performance

Strategies

Issues

Chapter 2 Chapter 5 Chapter 6 Chapter 7 Accounting, R&D, Chapter 9

and MIS Issues

Chapter 8

Perform

Internal Audit

Chapter 4

Chapter 11: Global/International Issues

Strategy Strategy Strategy

Formulation Implementation Evaluation

Source: Fred R. David, “How Companies Define Their Mission,” Long Range Planning 22, no. 3 (June 1988): 40.