Page 155 - Finance for Non-Financial Managers

P. 155

Siciliano08.qxd 2/8/2003 7:18 AM Page 136

136

Finance for Non-Financial Managers

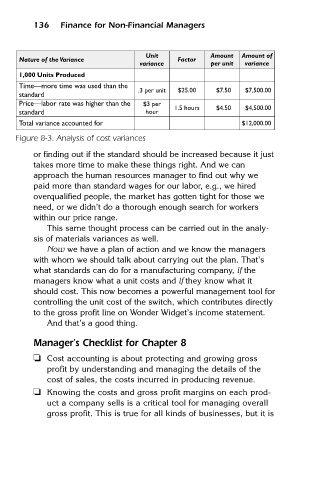

Unit

Nature of the Variance

variance

per unit

1,000 Units Produced variance Factor Amount Amount of

Time—more time was used than the

.3 per unit $25.00 $7.50 $7,500.00

standard

Price—labor rate was higher than the $3 per

1.5 hours $4.50 $4,500.00

standard hour

Total variance accounted for $12,000.00

Figure 8-3. Analysis of cost variances

or finding out if the standard should be increased because it just

takes more time to make these things right. And we can

approach the human resources manager to find out why we

paid more than standard wages for our labor, e.g., we hired

overqualified people, the market has gotten tight for those we

need, or we didn’t do a thorough enough search for workers

within our price range.

This same thought process can be carried out in the analy-

sis of materials variances as well.

Now we have a plan of action and we know the managers

with whom we should talk about carrying out the plan. That’s

what standards can do for a manufacturing company, if the

managers know what a unit costs and if they know what it

should cost. This now becomes a powerful management tool for

controlling the unit cost of the switch, which contributes directly

to the gross profit line on Wonder Widget’s income statement.

And that’s a good thing.

Manager’s Checklist for Chapter 8

❏ Cost accounting is about protecting and growing gross

profit by understanding and managing the details of the

cost of sales, the costs incurred in producing revenue.

❏ Knowing the costs and gross profit margins on each prod-

uct a company sells is a critical tool for managing overall

gross profit. This is true for all kinds of businesses, but it is