Page 154 - Finance for Non-Financial Managers

P. 154

Siciliano08.qxd 2/8/2003 7:18 AM Page 135

Cost Accounting

or differences from estab-

lished standards: price

tion A system of manage-

variances and usage vari- Management by excep- 135

ment in which standards

ances. Price variances are set for operating activities. The

occur when materials or actual results are then compared with

labor used in production those standards, and any differences

that are considered significant are

cost the company more

brought to the attention of the man-

per unit than was projected

agers, along with the reasons for the

when the standards were

differences and recommended correc-

set. Usage variances occur tive action, if appropriate.

when the production run

consumes more of the materials or labor than was planned.

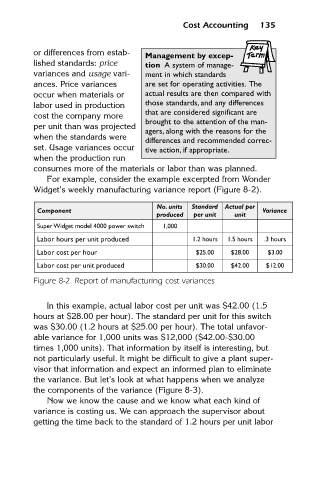

For example, consider the example excerpted from Wonder

Widget’s weekly manufacturing variance report (Figure 8-2).

No. units Standard Actual per

Component Variance

produced per unit unit

Super Widget model 4000 power switch 1,000

Labor hours per unit produced 1.2 hours 1.5 hours .3 hours

Labor cost per hour $25.00 $28.00 $3.00

Labor cost per unit produced $30.00 $42.00 $12.00

Figure 8-2. Report of manufacturing cost variances

In this example, actual labor cost per unit was $42.00 (1.5

hours at $28.00 per hour). The standard per unit for this switch

was $30.00 (1.2 hours at $25.00 per hour). The total unfavor-

able variance for 1,000 units was $12,000 ($42.00-$30.00

times 1,000 units). That information by itself is interesting, but

not particularly useful. It might be difficult to give a plant super-

visor that information and expect an informed plan to eliminate

the variance. But let’s look at what happens when we analyze

the components of the variance (Figure 8-3).

Now we know the cause and we know what each kind of

variance is costing us. We can approach the supervisor about

getting the time back to the standard of 1.2 hours per unit labor