Page 89 - Finance for Non-Financial Managers

P. 89

Siciliano05.qxd 2/8/2003 6:39 AM Page 70

Finance for Non-Financial Managers

70

for rent deposits, phone equipment, utility deposits, and a vari-

ety of related costs.

Closely related to the setup, and often happening simultane-

ously, is the purchase of assets to commence business opera-

tions. These include office equipment and computers for admin-

istrative purposes and factory equipment to begin manufactur-

ing widgets. For distributors, wholesalers, or retailers, those

costs would include equipping warehouse space in order to

stock the merchandise that that they will buy and resell.

The most important asset for any business is people, of

course, and Wonder Widget was probably hiring staff all along

the way toward the start of production—to answer phones, to

run the office, and to produce and sell their product. Of course,

this can get pretty expensive. If the owners had lots of cash,

they might have paid for all these things by simply writing a

check. Usually, however, prudent owners will choose to go to

their bank or a finance company of some kind to get an extend-

ed period of time to pay for their larger purchases, such as

machinery, furniture, and buildings.

That is where the company takes the next step in the cycle,

obtaining credit. The main purpose of credit in a growing busi-

ness is to enable the owners to increase the amount of capital

they have working for them by using creditors’ capital in addi-

tion to their own. This is called leverage, putting more capital to

work for the business, as discussed in Chapter 3.

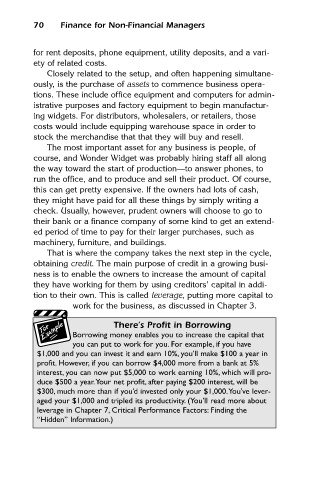

There’s Profit in Borrowing

Borrowing money enables you to increase the capital that

you can put to work for you. For example, if you have

$1,000 and you can invest it and earn 10%, you’ll make $100 a year in

profit. However, if you can borrow $4,000 more from a bank at 5%

interest, you can now put $5,000 to work earning 10%, which will pro-

duce $500 a year.Your net profit, after paying $200 interest, will be

$300, much more than if you’d invested only your $1,000.You’ve lever-

aged your $1,000 and tripled its productivity. (You’ll read more about

leverage in Chapter 7, Critical Performance Factors: Finding the

“Hidden” Information.)