Page 213 - How To Implement Lean Manufacturing

P. 213

Constraint Management 191

operating expenses but would increase revenues by over $26,000 per day. They were

making about 22 percent on sales, so this was extremely profitable, to say the least. The

plant manager was interested, but it was the policy of the company (that ugly word,

policy) that they would not increase manpower for any reason, above their current

levels. Hence, he no longer had the authority to add these people. Well, as you might

expect, there was a lot more to this experience … but this was not the first, nor the last,

time I encountered a business decision where “The Policy” was the system constraint.

These constraints are usually very costly and frequently the management is blind to

them and does not see them as constraints to the business.

The Economics of Constraints

The system constraint will limit the ability of the business to make money. However,

in most cases, if the constraint is broken, the resultant increase in production is often

the most profitable production the company has. Let’s look at a simple example of a

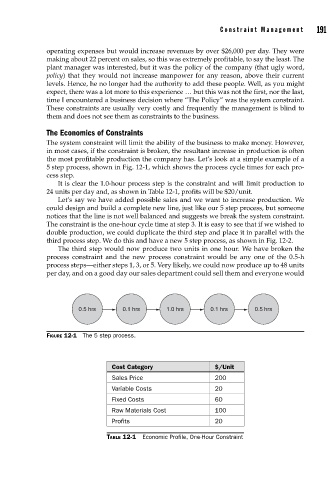

5 step process, shown in Fig. 12-1, which shows the process cycle times for each pro-

cess step.

It is clear the 1.0-hour process step is the constraint and will limit production to

24 units per day and, as shown in Table 12-1, profits will be $20/unit.

Let’s say we have added possible sales and we want to increase production. We

could design and build a complete new line, just like our 5 step process, but someone

notices that the line is not well balanced and suggests we break the system constraint.

The constraint is the one-hour cycle time at step 3. It is easy to see that if we wished to

double production, we could duplicate the third step and place it in parallel with the

third process step. We do this and have a new 5 step process, as shown in Fig. 12-2.

The third step would now produce two units in one hour. We have broken the

process constraint and the new process constraint would be any one of the 0.5-h

process steps—either steps 1, 3, or 5. Very likely, we could now produce up to 48 units

per day, and on a good day our sales department could sell them and everyone would

0.5 hrs 0.1 hrs 1.0 hrs 0.1 hrs 0.5 hrs

FIGURE 12-1 The 5 step process.

Cost Category $/Unit

Sales Price 200

Variable Costs 20

Fixed Costs 60

Raw Materials Cost 100

Profits 20

TABLE 12-1 Economic Profile, One-Hour Constraint