Page 226 -

P. 226

208 CHAPTER 6 The Production Process

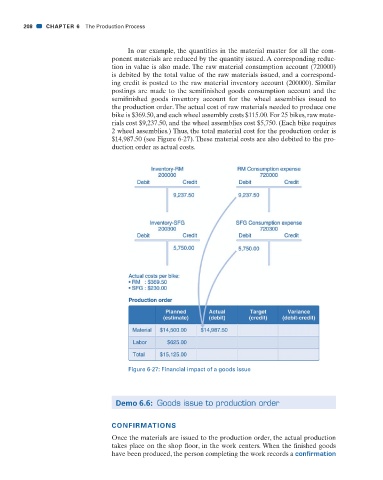

In our example, the quantities in the material master for all the com-

ponent materials are reduced by the quantity issued. A corresponding reduc-

tion in value is also made. The raw material consumption account (720000)

is debited by the total value of the raw materials issued, and a correspond-

ing credit is posted to the raw material inventory account (200000). Similar

postings are made to the semifi nished goods consumption account and the

semifi nished goods inventory account for the wheel assemblies issued to

the production order. The actual cost of raw materials needed to produce one

bike is $369.50, and each wheel assembly costs $115.00. For 25 bikes, raw mate-

rials cost $9,237.50, and the wheel assemblies cost $5,750. (Each bike requires

2 wheel assemblies.) Thus, the total material cost for the production order is

$14,987.50 (see Figure 6-27). These material costs are also debited to the pro-

duction order as actual costs.

Figure 6-27: Financial impact of a goods issue

Demo 6.6: Goods issue to production order

CONFIRMATIONS

Once the materials are issued to the production order, the actual production

takes place on the shop fl oor, in the work centers. When the fi nished goods

have been produced, the person completing the work records a confirmation

31/01/11 6:40 AM

CH006.indd 208

CH006.indd 208 31/01/11 6:40 AM