Page 275 - Water Loss Control

P. 275

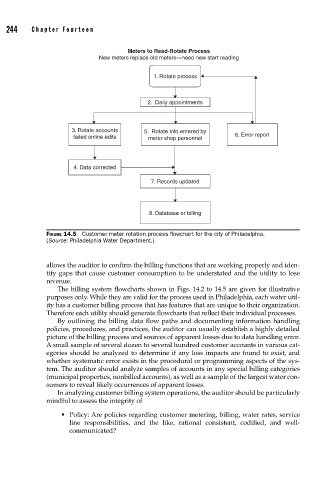

244 Cha pte r F o u r tee n

Meters to Read-Rotate Process

New meters replace old meters—need new start reading

1. Rotate process

2. Daily appointments

3. Rotate accounts 5. Rotate info entered by

failed online edits meter shop personnel 6. Error report

4. Data corrected

7. Records updated

8. Database or billing

FIGURE 14.5 Customer meter rotation process fl owchart for the city of Philadelphia.

(Source: Philadelphia Water Department.)

allows the auditor to confirm the billing functions that are working properly and iden-

tify gaps that cause customer consumption to be understated and the utility to lose

revenue.

The billing system flowcharts shown in Figs. 14.2 to 14.5 are given for illustrative

purposes only. While they are valid for the process used in Philadelphia, each water util-

ity has a customer billing process that has features that are unique to their organization.

Therefore each utility should generate flowcharts that reflect their individual processes.

By outlining the billing data flow paths and documenting information handling

policies, procedures, and practices, the auditor can usually establish a highly detailed

picture of the billing process and sources of apparent losses due to data handling error.

A small sample of several dozen to several hundred customer accounts in various cat-

egories should be analyzed to determine if any loss impacts are found to exist, and

whether systematic error exists in the procedural or programming aspects of the sys-

tem. The auditor should analyze samples of accounts in any special billing categories

(municipal properties, nonbilled accounts), as well as a sample of the largest water con-

sumers to reveal likely occurrences of apparent losses.

In analyzing customer billing system operations, the auditor should be particularly

mindful to assess the integrity of

• Policy: Are policies regarding customer metering, billing, water rates, service

line responsibilities, and the like, rational consistent, codified, and well-

communicated?