Page 149 - Accounting Information Systems

P. 149

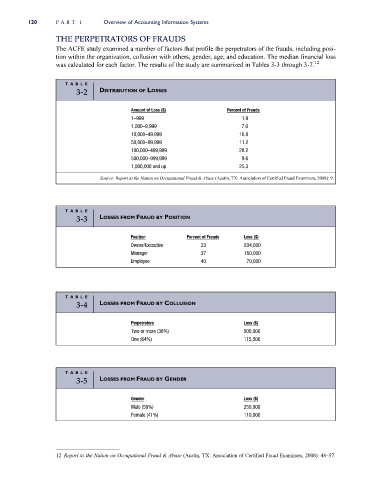

120 PART I Overview of Accounting Information Systems

THE PERPETRATORS OF FRAUDS

The ACFE study examined a number of factors that profile the perpetrators of the frauds, including posi-

tion within the organization, collusion with others, gender, age, and education. The median financial loss

was calculated for each factor. The results of the study are summarized in Tables 3-3 through 3-7. 12

TAB L E

3-2 DISTRIBUTION OF LOSSES

Amount of Loss ($) Percent of Frauds

1–999 1.9

1,000–9,999 7.0

10,000–49,999 16.8

50,000–99,999 11.2

100,000–499,999 28.2

500,000–999,999 9.6

1,000,000 and up 25.3

Source: Report to the Nation on Occupational Fraud & Abuse (Austin, TX: Association of Certified Fraud Examiners, 2008): 9.

TAB L E

3-3 LOSSES FROM FRAUD BY POSITION

Position Percent of Frauds Loss ($)

Owner/Executive 23 834,000

Manager 37 150,000

Employee 40 70,000

TAB L E

3-4 LOSSES FROM FRAUD BY COLLUSION

Perpetrators Loss ($)

Two or more (36%) 500,000

One (64%) 115,500

TAB L E

3-5 LOSSES FROM FRAUD BY GENDER

Gender Loss ($)

Male (59%) 250,000

Female (41%) 110,000

12 Report to the Nation on Occupational Fraud & Abuse (Austin, TX: Association of Certified Fraud Examiners, 2008): 48–57.