Page 185 - Accounting Information Systems

P. 185

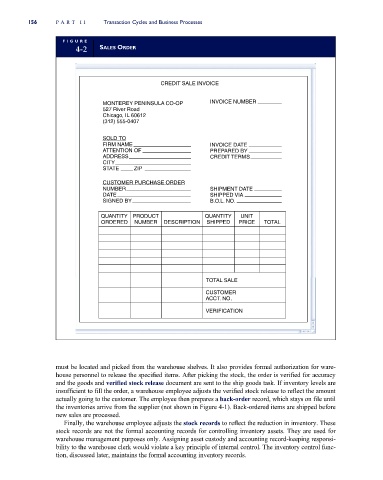

156 PART II Transaction Cycles and Business Processes

FI GU RE

4-2 SALES ORDER

CREDIT SALE INVOICE

MONTEREY PENINSULA CO-OP INVOICE NUMBER

527 River Road

Chicago, IL 60612

(312) 555-0407

SOLD TO

FIRM NAME INVOICE DATE

ATTENTION OF PREPARED BY

ADDRESS CREDIT TERMS

CITY

STATE ZIP

CUSTOMER PURCHASE ORDER

NUMBER SHIPMENT DATE

DATE SHIPPED VIA

SIGNED BY B.O.L. NO.

QUANTITY PRODUCT QUANTITY UNIT

ORDERED NUMBER DESCRIPTION SHIPPED PRICE TOTAL

TOTAL SALE

CUSTOMER

ACCT. NO.

VERIFICATION

must be located and picked from the warehouse shelves. It also provides formal authorization for ware-

house personnel to release the specified items. After picking the stock, the order is verified for accuracy

and the goods and verified stock release document are sent to the ship goods task. If inventory levels are

insufficient to fill the order, a warehouse employee adjusts the verified stock release to reflect the amount

actually going to the customer. The employee then prepares a back-order record, which stays on file until

the inventories arrive from the supplier (not shown in Figure 4-1). Back-ordered items are shipped before

new sales are processed.

Finally, the warehouse employee adjusts the stock records to reflect the reduction in inventory. These

stock records are not the formal accounting records for controlling inventory assets. They are used for

warehouse management purposes only. Assigning asset custody and accounting record-keeping responsi-

bility to the warehouse clerk would violate a key principle of internal control. The inventory control func-

tion, discussed later, maintains the formal accounting inventory records.