Page 40 - Accounting Information Systems

P. 40

C H A P TER 1 The Information System: An Accountant’s Perspective 11

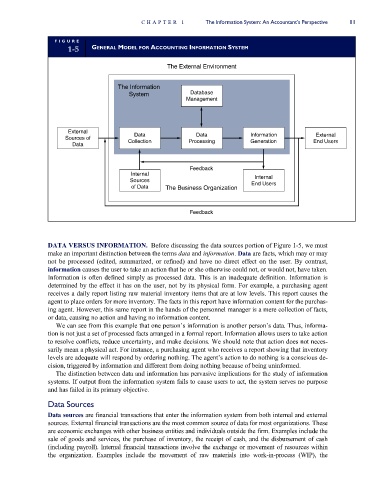

FI G U R E

1-5 GENERAL MODEL FOR ACCOUNTING INFORMATION SYSTEM

The External Environment

The Information

System Database

Management

External

External

Data

Data

Sources of Collection Processing Information End Users

Generation

Data

Feedback

Internal

Sources Internal

of Data The Business Organization End Users

Feedback

DATA VERSUS INFORMATION. Before discussing the data sources portion of Figure 1-5, we must

make an important distinction between the terms data and information. Data are facts, which may or may

not be processed (edited, summarized, or refined) and have no direct effect on the user. By contrast,

information causes the user to take an action that he or she otherwise could not, or would not, have taken.

Information is often defined simply as processed data. This is an inadequate definition. Information is

determined by the effect it has on the user, not by its physical form. For example, a purchasing agent

receives a daily report listing raw material inventory items that are at low levels. This report causes the

agent to place orders for more inventory. The facts in this report have information content for the purchas-

ing agent. However, this same report in the hands of the personnel manager is a mere collection of facts,

or data, causing no action and having no information content.

We can see from this example that one person’s information is another person’s data. Thus, informa-

tion is not just a set of processed facts arranged in a formal report. Information allows users to take action

to resolve conflicts, reduce uncertainty, and make decisions. We should note that action does not neces-

sarily mean a physical act. For instance, a purchasing agent who receives a report showing that inventory

levels are adequate will respond by ordering nothing. The agent’s action to do nothing is a conscious de-

cision, triggered by information and different from doing nothing because of being uninformed.

The distinction between data and information has pervasive implications for the study of information

systems. If output from the information system fails to cause users to act, the system serves no purpose

and has failed in its primary objective.

Data Sources

Data sources are financial transactions that enter the information system from both internal and external

sources. External financial transactions are the most common source of data for most organizations. These

are economic exchanges with other business entities and individuals outside the firm. Examples include the

sale of goods and services, the purchase of inventory, the receipt of cash, and the disbursement of cash

(including payroll). Internal financial transactions involve the exchange or movement of resources within

the organization. Examples include the movement of raw materials into work-in-process (WIP), the