Page 211 - Essentials of Payroll: Management and Accounting

P. 211

ESSENTIALS of Payr oll: Management and Accounting

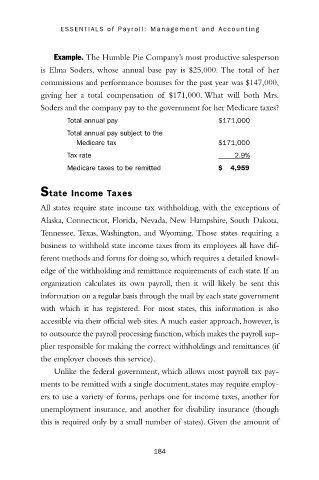

Example. The Humble Pie Company’s most productive salesperson

is Elma Soders, whose annual base pay is $25,000. The total of her

commissions and performance bonuses for the past year was $147,000,

giving her a total compensation of $171,000. What will both Mrs.

Soders and the company pay to the government for her Medicare taxes?

Total annual pay $171,000

Total annual pay subject to the

Medicare tax $171,000

Tax rate 2.9%

Medicare taxes to be remitted $ 4,959

State Income Taxes

All states require state income tax withholding, with the exceptions of

Alaska, Connecticut, Florida, Nevada, New Hampshire, South Dakota,

Tennessee, Texas, Washington, and Wyoming. Those states requiring a

business to withhold state income taxes from its employees all have dif-

ferent methods and forms for doing so, which requires a detailed knowl-

edge of the withholding and remittance requirements of each state. If an

organization calculates its own payroll, then it will likely be sent this

information on a regular basis through the mail by each state government

with which it has registered. For most states, this information is also

accessible via their official web sites.A much easier approach, however, is

to outsource the payroll processing function,which makes the payroll sup-

plier responsible for making the correct withholdings and remittances (if

the employer chooses this service).

Unlike the federal government, which allows most payroll tax pay-

ments to be remitted with a single document,states may require employ-

ers to use a variety of forms, perhaps one for income taxes, another for

unemployment insurance, and another for disability insurance (though

this is required only by a small number of states). Given the amount of

184