Page 170 - Sustainability Communication Interdisciplinary Perspectives and Theoritical Foundations

P. 170

14 Corporate Sustainability Reporting 153

Finally, with the collection and analysis of information as well as the creation of

greater transparency, sustainability reporting can support internal information and

control processes. Seen as a learning rather than an adaptive process, sustainability

reporting may also initiate processes to enhance employees and manager aware-

ness and motivation, and lead to individual and organisational changes that foster

organisational performance. This requires critically reflexive processes where

accepted rules, strategies and norms are questioned and improved (Gond and

Herrbach 2006).

Which of these goals and benefits motivate management most to deal with sus-

tainability reporting depends on the company-specific situation, on industry and

market conditions, as well as on stakeholder constellations and management prefer-

ences. Moreover, since reporting initiatives convey a picture of corporate respon-

siveness to key societal concerns, they have changed over the last decades. Their

historical development is described next.

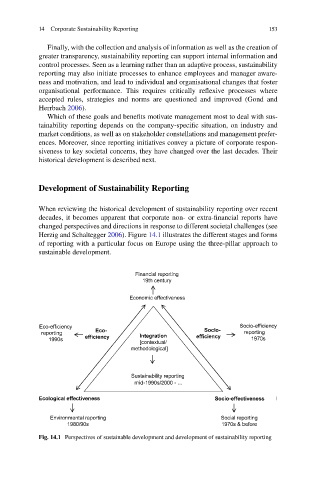

Development of Sustainability Reporting

When reviewing the historical development of sustainability reporting over recent

decades, it becomes apparent that corporate non- or extra-financial reports have

changed perspectives and directions in response to different societal challenges (see

Herzig and Schaltegger 2006). Figure 14.1 illustrates the different stages and forms

of reporting with a particular focus on Europe using the three-pillar approach to

sustainable development.

Fig. 14.1 Perspectives of sustainable development and development of sustainability reporting