Page 112 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 112

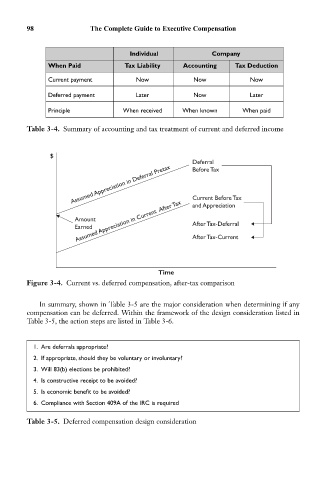

98 The Complete Guide to Executive Compensation

Individual Company

When Paid Tax Liability Accounting Tax Deduction

Current payment Now Now Now

Deferred payment Later Now Later

Principle When received When known When paid

Table 3-4. Summary of accounting and tax treatment of current and deferred income

$

Deferral

Assumed Appreciation in Deferral Pretax Current Before Tax

Before Tax

Assumed Appreciation in Current After Tax

Amount and Appreciation

Earned After Tax-Deferral

After Tax-Current

Time

Figure 3-4. Current vs. deferred compensation, after-tax comparison

In summary, shown in Table 3-5 are the major consideration when determining if any

compensation can be deferred. Within the framework of the design consideration listed in

Table 3-5, the action steps are listed in Table 3-6.

1. Are deferrals appropriate?

2. If appropriate, should they be voluntary or involuntary?

3. Will 83(b) elections be prohibited?

4. Is constructive receipt to be avoided?

5. Is economic benefit to be avoided?

6. Compliance with Section 409A of the IRC is required

Table 3-5. Deferred compensation design consideration