Page 468 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 468

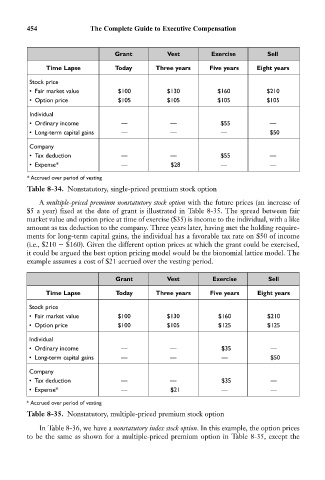

454 The Complete Guide to Executive Compensation

Grant Vest Exercise Sell

Time Lapse Today Three years Five years Eight years

Stock price

• Fair market value $100 $130 $160 $210

• Option price $105 $105 $105 $105

Individual

• Ordinary income — — $55 —

• Long-term capital gains — — — $50

Company

• Tax deduction — — $55 —

• Expense* — $28 — —

* Accrued over period of vesting

Table 8-34. Nonstatutory, single-priced premium stock option

A multiple-priced premium nonstatutory stock option with the future prices (an increase of

$5 a year) fixed at the date of grant is illustrated in Table 8-35. The spread between fair

market value and option price at time of exercise ($35) is income to the individual, with a like

amount as tax deduction to the company. Three years later, having met the holding require-

ments for long-term capital gains, the individual has a favorable tax rate on $50 of income

(i.e., $210 $160). Given the different option prices at which the grant could be exercised,

it could be argued the best option pricing model would be the bionomial lattice model. The

example assumes a cost of $21 accrued over the vesting period.

Grant Vest Exercise Sell

Time Lapse Today Three years Five years Eight years

Stock price

• Fair market value $100 $130 $160 $210

• Option price $100 $105 $125 $125

Individual

• Ordinary income — — $35 —

• Long-term capital gains — — — $50

Company

• Tax deduction — — $35 —

• Expense* — $21 — —

* Accrued over period of vesting

Table 8-35. Nonstatutory, multiple-priced premium stock option

In Table 8-36, we have a nonstatutory index stock option. In this example, the option prices

to be the same as shown for a multiple-priced premium option in Table 8-35, except the