Page 645 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 645

630 The Complete Guide to Executive Compensation

Probably most important of all, boards and their compensation committees are realizing

that executive pay programs are a means to an end and not an end unto themselves. They

are sometimes complicated and too often don’t work well, but they are the best technique

available for ensuring that shareholder interests are placed in proper focus.

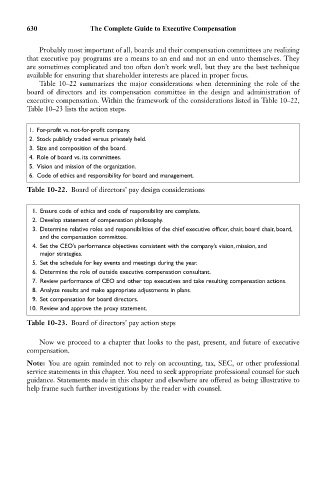

Table 10–22 summarizes the major considerations when determining the role of the

board of directors and its compensation committee in the design and administration of

executive compensation. Within the framework of the considerations listed in Table 10–22,

Table 10–23 lists the action steps.

1. For-profit vs. not-for-profit company.

2. Stock publicly traded versus privately held.

3. Size and composition of the board.

4. Role of board vs. its committees.

5. Vision and mission of the organization.

6. Code of ethics and responsibility for board and management.

Table 10-22. Board of directors’ pay design considerations

1. Ensure code of ethics and code of responsibility are complete.

2. Develop statement of compensation philosophy.

3. Determine relative roles and responsibilities of the chief executive officer, chair, board chair, board,

and the compensation committee.

4. Set the CEO’s performance objectives consistent with the company’s vision, mission, and

major strategies.

5. Set the schedule for key events and meetings during the year.

6. Determine the role of outside executive compensation consultant.

7. Review performance of CEO and other top executives and take resulting compensation actions.

8. Analyze results and make appropriate adjustments in plans.

9. Set compensation for board directors.

10. Review and approve the proxy statement.

Table 10-23. Board of directors’ pay action steps

Now we proceed to a chapter that looks to the past, present, and future of executive

compensation.

Note: You are again reminded not to rely on accounting, tax, SEC, or other professional

service statements in this chapter. You need to seek appropriate professional counsel for such

guidance. Statements made in this chapter and elsewhere are offered as being illustrative to

help frame such further investigations by the reader with counsel.