Page 236 - Computational Statistics Handbook with MATLAB

P. 236

Chapter 6: Monte Carlo Methods for Inferential Statistics 223

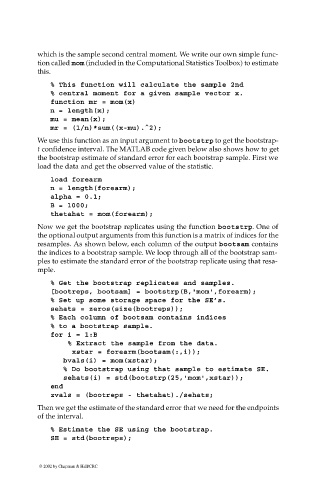

which is the sample second central moment. We write our own simple func-

tion called mom (included in the Computational Statistics Toolbox) to estimate

this.

% This function will calculate the sample 2nd

% central moment for a given sample vector x.

function mr = mom(x)

n = length(x);

mu = mean(x);

mr = (1/n)*sum((x-mu).^2);

We use this function as an input argument to bootstrp to get the bootstrap-

t confidence interval. The MATLAB code given below also shows how to get

the bootstrap estimate of standard error for each bootstrap sample. First we

load the data and get the observed value of the statistic.

load forearm

n = length(forearm);

alpha = 0.1;

B = 1000;

thetahat = mom(forearm);

Now we get the bootstrap replicates using the function bootstrp. One of

the optional output arguments from this function is a matrix of indices for the

resamples. As shown below, each column of the output bootsam contains

the indices to a bootstrap sample. We loop through all of the bootstrap sam-

ples to estimate the standard error of the bootstrap replicate using that resa-

mple.

% Get the bootstrap replicates and samples.

[bootreps, bootsam] = bootstrp(B,'mom',forearm);

% Set up some storage space for the SE’s.

sehats = zeros(size(bootreps));

% Each column of bootsam contains indices

% to a bootstrap sample.

for i = 1:B

% Extract the sample from the data.

xstar = forearm(bootsam(:,i));

bvals(i) = mom(xstar);

% Do bootstrap using that sample to estimate SE.

sehats(i) = std(bootstrp(25,'mom',xstar));

end

zvals = (bootreps - thetahat)./sehats;

Then we get the estimate of the standard error that we need for the endpoints

of the interval.

% Estimate the SE using the bootstrap.

SE = std(bootreps);

© 2002 by Chapman & Hall/CRC