Page 55 - Essentials of Payroll: Management and Accounting

P. 55

ESSENTIALS of Payr oll: Management and Accounting

elaborate tracking mechanisms for these two cost categories, while over-

head costs were largely ignored.Since the advent of technology advances,

however, the cost of overhead has skyrocketed, while direct labor costs

have shrunk.As a result, much of the accounting literature has advocated

the complete elimination of direct labor cost tracking, on the grounds

that the tracking mechanism is much too expensive in relation to the

amount of direct labor cost that is now incurred.

In reality, a company’s specific circumstances may still require the use

of detailed direct labor tracking.This is certainly the case if the proportion

of direct labor to total company costs remains high, such as 30 percent

or more of total company costs. Given this large percentage, it is crucial

that management know the variances that are being incurred and how to

reduce them. Another case is when a company operates in such a com-

petitive industry that shifts in costs of as little as 1 percent will have a

drastic impact on overall profitability. Finally, the decision to use a

detailed labor-tracking mechanism can be driven less by the total direct

labor cost and more by the level of efficiency of the tracking system.

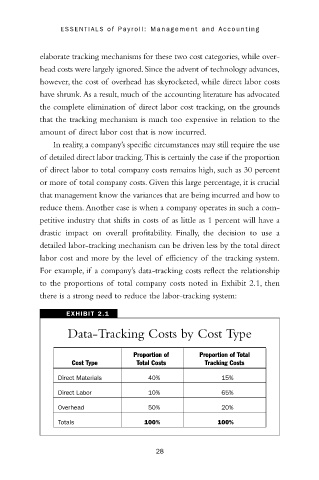

For example, if a company’s data-tracking costs reflect the relationship

to the proportions of total company costs noted in Exhibit 2.1, then

there is a strong need to reduce the labor-tracking system:

EXHIBIT 2.1

Data-Tracking Costs by Cost Type

Proportion of Proportion of Total

Cost Type Total Costs Tracking Costs

Direct Materials 40% 15%

Direct Labor 10% 65%

Overhead 50% 20%

Totals 100% 100%

28