Page 122 - Finance for Non-Financial Managers

P. 122

Siciliano07.qxd 3/20/2003 11:23 AM Page 103

Critical Performance Factors

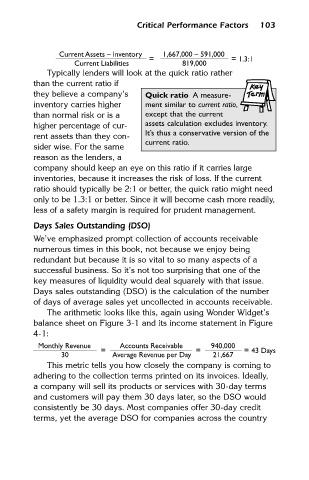

1,667,000 – 591,000

Current Assets – Inventory

=

Current Liabilities

819,000

Typically lenders will look at the quick ratio rather = 1.3:1 103

than the current ratio if

they believe a company’s Quick ratio A measure-

inventory carries higher ment similar to current ratio,

than normal risk or is a except that the current

higher percentage of cur- assets calculation excludes inventory.

rent assets than they con- It’s thus a conservative version of the

current ratio.

sider wise. For the same

reason as the lenders, a

company should keep an eye on this ratio if it carries large

inventories, because it increases the risk of loss. If the current

ratio should typically be 2:1 or better, the quick ratio might need

only to be 1.3:1 or better. Since it will become cash more readily,

less of a safety margin is required for prudent management.

Days Sales Outstanding (DSO)

We’ve emphasized prompt collection of accounts receivable

numerous times in this book, not because we enjoy being

redundant but because it is so vital to so many aspects of a

successful business. So it’s not too surprising that one of the

key measures of liquidity would deal squarely with that issue.

Days sales outstanding (DSO) is the calculation of the number

of days of average sales yet uncollected in accounts receivable.

The arithmetic looks like this, again using Wonder Widget’s

balance sheet on Figure 3-1 and its income statement in Figure

4-1:

Monthly Revenue Accounts Receivable 940,000

= = = 43 Days

30 Average Revenue per Day 21,667

This metric tells you how closely the company is coming to

adhering to the collection terms printed on its invoices. Ideally,

a company will sell its products or services with 30-day terms

and customers will pay them 30 days later, so the DSO would

consistently be 30 days. Most companies offer 30-day credit

terms, yet the average DSO for companies across the country