Page 346 - Orlicky's Material Requirements Planning

P. 346

CHAPTER 19 Repetitive Manufacturing Application 325

practice to follow in a repetitive or process industry. Rarely is labor a variable cost for the

product. Labor in such organization tends to be fixed in the short term.

PERIOD COSTING

A steady level of work-in-process and a reliably short throughput time make period cost-

ing possible. Work-in-process is directly related to lead time. When lead time stays con-

stant, then so does the level of work-in-process. Keeping track of every detailed transac-

tion costs more than the value of the information received. Statistical process control

charts can be used to track costs over time. Using the same rules as would be used when

managing part dimensions, costs can be expected to vary within a certain tolerance.

When the trend begins to move out of control or a special occurrence happens to cause a

one-time spike in cost, this can be identified quickly. This kind of reporting is now avail-

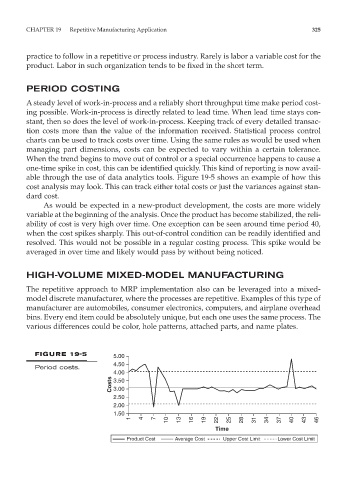

able through the use of data analytics tools. Figure 19-5 shows an example of how this

cost analysis may look. This can track either total costs or just the variances against stan-

dard cost.

As would be expected in a new-product development, the costs are more widely

variable at the beginning of the analysis. Once the product has become stabilized, the reli-

ability of cost is very high over time. One exception can be seen around time period 40,

when the cost spikes sharply. This out-of-control condition can be readily identified and

resolved. This would not be possible in a regular costing process. This spike would be

averaged in over time and likely would pass by without being noticed.

HIGH-VOLUME MIXED-MODEL MANUFACTURING

The repetitive approach to MRP implementation also can be leveraged into a mixed-

model discrete manufacturer, where the processes are repetitive. Examples of this type of

manufacturer are automobiles, consumer electronics, computers, and airplane overhead

bins. Every end item could be absolutely unique, but each one uses the same process. The

various differences could be color, hole patterns, attached parts, and name plates.

FIGURE 19-5 5.00

4.50

Period costs.

4.00

Costs 3.50

3.00

2.50

2.00

1.50

10 13 16 19 22 25 28 31 34 37 40 43 46

1 4 7

Time

Product Cost Average Cost Upper Cost Limit Lower Cost Limit