Page 95 -

P. 95

CHAPTER 3 • THE EXTERNAL ASSESSMENT 61

The Nature of an External Audit

The purpose of an external audit is to develop a finite list of opportunities that could

benefit a firm and threats that should be avoided. As the term finite suggests, the external

audit is not aimed at developing an exhaustive list of every possible factor that could

influence the business; rather, it is aimed at identifying key variables that offer actionable

responses. Firms should be able to respond either offensively or defensively to the factors

by formulating strategies that take advantage of external opportunities or that minimize

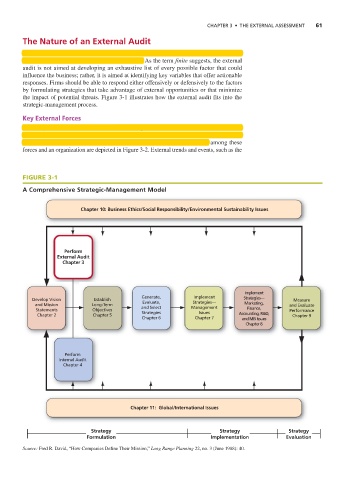

the impact of potential threats. Figure 3-1 illustrates how the external audit fits into the

strategic-management process.

Key External Forces

External forces can be divided into five broad categories: (1) economic forces; (2) social, cul-

tural, demographic, and natural environment forces; (3) political, governmental, and legal

forces; (4) technological forces; and (5) competitive forces. Relationships among these

forces and an organization are depicted in Figure 3-2. External trends and events, such as the

FIGURE 3-1

A Comprehensive Strategic-Management Model

Chapter 10: Business Ethics/Social Responsibility/Environmental Sustainability Issues

Perform

External Audit

Chapter 3

Implement

Generate, Implement Strategies—

Develop Vision Establish Evaluate, Strategies— Measure

and Mission Long-Term Marketing, and Evaluate

and Select Management Finance,

Statements Objectives Strategies Issues Performance

Chapter 2 Chapter 5 Accounting, R&D, Chapter 9

Chapter 6 Chapter 7 and MIS Issues

Chapter 8

Perform

Internal Audit

Chapter 4

Chapter 11: Global/International Issues

Strategy Strategy Strategy

Formulation Implementation Evaluation

Source: Fred R. David, “How Companies Define Their Mission,” Long Range Planning 22, no. 3 (June 1988): 40.