Page 80 - Accounting Information Systems

P. 80

CHAPT E R 2 Introduction to Transaction Processing 51

FI G U R E

2-10 RELATIONSHIP BETWEEN THE SUBSIDIARY LEDGER AND THE GENERAL LEDGER

Accounts Receivable

General Ledger

Subsidiary Ledger

Hobbs Johnson Cash

XXXX.XX XXXX.XX

9,845,260

Smith

XXXX.XX

Total AR = Accounts Receivable

14,205,800

14,205,800

Ray Howard

XXXX.XX XXXX.XX

Inventory

126,389,538

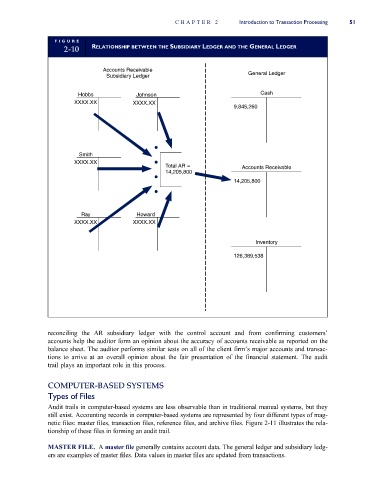

reconciling the AR subsidiary ledger with the control account and from confirming customers’

accounts help the auditor form an opinion about the accuracy of accounts receivable as reported on the

balance sheet. The auditor performs similar tests on all of the client firm’s major accounts and transac-

tions to arrive at an overall opinion about the fair presentation of the financial statement. The audit

trail plays an important role in this process.

COMPUTER-BASED SYSTEMS

Types of Files

Audit trails in computer-based systems are less observable than in traditional manual systems, but they

still exist. Accounting records in computer-based systems are represented by four different types of mag-

netic files: master files, transaction files, reference files, and archive files. Figure 2-11 illustrates the rela-

tionship of these files in forming an audit trail.

MASTER FILE. A master file generally contains account data. The general ledger and subsidiary ledg-

ers are examples of master files. Data values in master files are updated from transactions.