Page 69 - Chemical process engineering design and economics

P. 69

54 Chapter 2

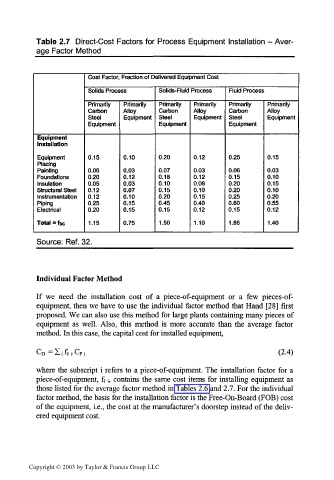

Table 2.7 Direct-Cost Factors for Process Equipment Installation - Aver-

age Factor Method _______

Cost Factor, Fraction of Delivered Equipment Cost

Solids Process Solids-Fluid Process Fluid Process

Primarily Primarily Primarily Primarily Primarily Primarily

Carbon Alloy Carbon Alloy Carbon Alloy

Steel Equipment Steel Equipment Steel Equipment

Equipment Equipment Equipment

Equipment

Installation

Equipment 0.15 0.10 0.20 0.12 0.25 0.15

Placing

Painting 0.06 0.03 0.07 0.03 0.06 0.03

Foundations 0.20 0.12 0.18 0.12 0.15 0.10

Insulation 0.05 0.03 0.10 0.06 0.20 0.15

Structural Steel 0.12 0.07 0.15 0.10 0.20 0.10

Instrumentation 0.12 0.10 0.20 0.15 0.25 0.20

Piping 0.25 0.15 0.45 0.40 0.60 0.55

Electrical 0.20 0.15 0.15 0.12 0.15 0.12

Total = foe 1.15 0.75 1.50 1.10 1.86 1.40

Source: Ref. 32.

Individual Factor Method

If we need the installation cost of a piece-of-equipment or a few pieces-of-

equipment, then we have to use the individual factor method that Hand [28] first

proposed. We can also use this method for large plants containing many pieces of

equipment as well. Also, this method is more accurate than the average factor

method. In this case, the capital cost for installed equipment,

CD = S; fi i C P (2.4)

where the subscript i refers to a piece-of-equipment. The installation factor for a

piece-of-equipment, f\;, contains the same cost items for installing equipment as

those listed for the average factor method in Tables 2.6 and 2.7. For the individual

factor method, the basis for the installation factor is the Free-On-Board (FOB) cost

of the equipment, i.e., the cost at the manufacturer's doorstep instead of the deliv-

ered equipment cost.

Copyright © 2003 by Taylor & Francis Group LLC