Page 230 - Mechatronics for Safety, Security and Dependability in a New Era

P. 230

Ch44-I044963.fm Page 214 Tuesday, August 1, 2006 4:00 PM

Ch44-I044963.fm

214

214 Page 214 Tuesday, August 1, 2006 4:00 PM

Algorithm based approach. And their performance and characteristics are investigated through

experiments with a Distributed Virtual Factory[2,3].

2. PRODUCT COST ANALYSIS

To evaluate and estimate the product cost and its composition, variety of accounting method has

been proposed. In recent manufacturing systems, the share of indirect costs in the total cost is

relatively increasing due to the development of the automation and IT. And it becomes more and

more important to reduce and control the indirect costs. Respecting the back ground, we employ

ABC, since the indirect costs are reasonably distributed with ABC compared with the other

accounting methods.

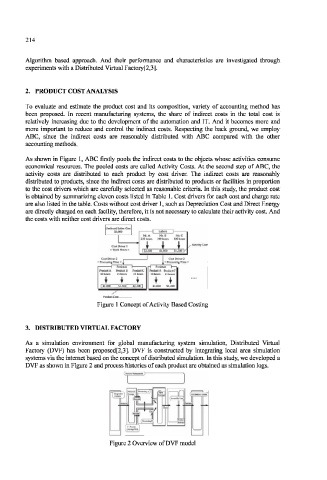

As shown in Figure 1, ABC firstly pools the indirect costs to the objects whose activities consume

economical resources. The pooled costs are called Activity Costs. At the second step of ABC, the

activity costs are distributed to each product by cost driver. The indirect costs are reasonably

distributed to products, since the indirect costs are distributed to products or facilities in proportion

to the cost drivers which are carefully selected as reasonable criteria. In this study, the product cost

is obtained by summarizing eleven costs listed in Table 1. Cost drivers for each cost and charge rate

are also listed in the table. Costs without cost driver 1, such as Depreciation Cost and Direct Energy

are directly charged on each facility, therefore, it is not necessary to calculate their activity cost. And

the costs with neither cost drivers are direct costs.

(Ind eel) Labor Cost

1 L3C < " '

Mr. A Mr B Mr. C

1 fc> 250 hours 100 ours 150 hours j Activity C

Cost Driver 1 rgBdg jsi KM _8J j 5gLK

Work Hours =

1

Cost Driver 2 Cost Driver 2

= Processing Time = I

Product A Product B ProductC Product A Produci C I

10 hours 13 hours 12 hours 10 hours 12 hours 1

I I

*

11 m 51,300 SI ,20 VJ $1,200 |

Figure 1 Concept of Activity Based Costing

3. DISTRIBUTED VIRTUAL FACTORY

As a simulation environment for global manufacturing system simulation, Distributed Virtual

Factory (DVF) has been proposed[2,3]. DVF is constructed by integrating local area simulation

systems via the internet based on the concept of distributed simulation. In this study, we developed a

DVF as shown in Figure 2 and process histories of each product are obtained as simulation logs.

Figure 2 Overview of DVF model