Page 321 -

P. 321

CHAPTER 9 • STRATEGY REVIEW, EVALUATION, AND CONTROL 287

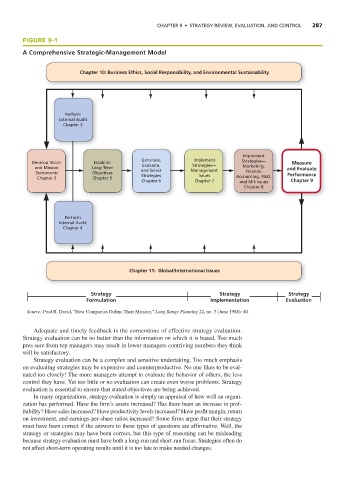

FIGURE 9-1

A Comprehensive Strategic-Management Model

Chapter 10: Business Ethics, Social Responsibility, and Environmental Sustainability

Perform

External Audit

Chapter 3

Implement

Generate, Implement Strategies—

Develop Vision Establish Evaluate, Strategies— Measure

and Mission Long-Term Marketing, and Evaluate

Statements Objectives and Select Management Finance, Performance

Strategies

Issues

Chapter 2 Chapter 5 Accounting, R&D,

Chapter 6 Chapter 7 and MIS Issues Chapter 9

Chapter 8

Perform

Internal Audit

Chapter 4

Chapter 11: Global/International Issues

Strategy Strategy Strategy

Formulation Implementation Evaluation

Source: Fred R. David, “How Companies Define Their Mission,” Long Range Planning 22, no. 3 (June 1988): 40.

Adequate and timely feedback is the cornerstone of effective strategy evaluation.

Strategy evaluation can be no better than the information on which it is based. Too much

pres sure from top managers may result in lower managers contriving numbers they think

will be satisfactory.

Strategy evaluation can be a complex and sensitive undertaking. Too much emphasis

on evaluating strategies may be expensive and counterproductive. No one likes to be eval-

uated too closely! The more managers attempt to evaluate the behavior of others, the less

control they have. Yet too little or no evaluation can create even worse problems. Strategy

evaluation is essential to ensure that stated objectives are being achieved.

In many organizations, strategy evaluation is simply an appraisal of how well an organi-

zation has performed. Have the firm’s assets increased? Has there been an increase in prof-

itability? Have sales increased? Have productivity levels increased? Have profit margin, return

on investment, and earnings-per-share ratios increased? Some firms argue that their strategy

must have been correct if the answers to these types of questions are affirmative. Well, the

strategy or strategies may have been correct, but this type of reasoning can be misleading

because strategy evaluation must have both a long-run and short-run focus. Strategies often do

not affect short-term operating results until it is too late to make needed changes.