Page 577 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 577

Chapter 9. Design and Communication Considerations 563

practices should have been conducted, but coverage in the business press is another

reason to determine whether the policy is still appropriate or needs modification.

7. What impact does a sudden change in company profitability have on the executive

pay plans. An unforeseen problem with a major product or loss of a major customer

is likely to have a dramatic effect on both short- and long-term profitability of the

company and requires an immediate review of the pay plans. Plan focus must be on how

to optimize results given the negative factors. Cash and especially restricted stock awards

tied to specific performance targets should be given significant consideration.

8. What impact does a company drifting into decline have on pay plans? As described

in this book, each stage of the market cycle has its own compensation element profile.

The decline stage is primarily cash-based incentives, because stock values are declining.

But if the company has specific plans for a turnaround to reposition the company into a

growth company, then stock options should be a major component.

This list of questions is intended to be representative (not exhaustive) and hopefully

helpful in stimulating thinking of additional considerations that must be addressed.

STRUCTURING PAY RELATIONSHIPS

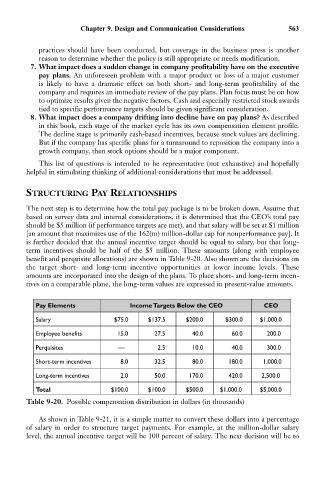

The next step is to determine how the total pay package is to be broken down. Assume that

based on survey data and internal considerations, it is determined that the CEO’s total pay

should be $5 million (if performance targets are met), and that salary will be set at $1 million

[an amount that maximizes use of the 162(m) million-dollar cap for nonperformance pay]. It

is further decided that the annual incentive target should be equal to salary, but that long-

term incentives should be half of the $5 million. These amounts (along with employee

benefit and perquisite allocations) are shown in Table 9-20. Also shown are the decisions on

the target short- and long-term incentive opportunities at lower income levels. These

amounts are incorporated into the design of the plans. To place short- and long-term incen-

tives on a comparable plane, the long-term values are expressed in present-value amounts.

Pay Elements Income Targets Below the CEO CEO

Salary $75.0 $137.5 $200.0 $300.0 $1,000.0

Employee benefits 15.0 27.5 40.0 60.0 200.0

Perquisites — 2.5 10.0 40.0 300.0

Short-term incentives 8.0 32.5 80.0 180.0 1,000.0

Long-term incentives 2.0 50.0 170.0 420.0 2,500.0

Total $100.0 $100.0 $500.0 $1,000.0 $5,000.0

Table 9-20. Possible compensation distribution in dollars (in thousands)

As shown in Table 9-21, it is a simple matter to convert these dollars into a percentage

of salary in order to structure target payments. For example, at the million-dollar salary

level, the annual incentive target will be 100 percent of salary. The next decision will be to