Page 337 - Fluid Power Engineering

P. 337

Financial Modeling of W ind Projects 297

Lender

Int+Princ

Wind

Developer Tax Investor

Wind

Project

Energy Output, X 1 %

kWh

kWh*(PPA+REC) kWh*PTC

100-X 1 %

Revenue, PTC

Rev

Rev-OE-Int-Dep

Rev-OE X 2 %

Taxable

Income, TI

EBITDA

TI*TR

EBITDA-Int-Princ-Tax

Tax Gain/

100-X 2 % X 3 %

Loss

100-X 3 %

After-tax

Cash Flow

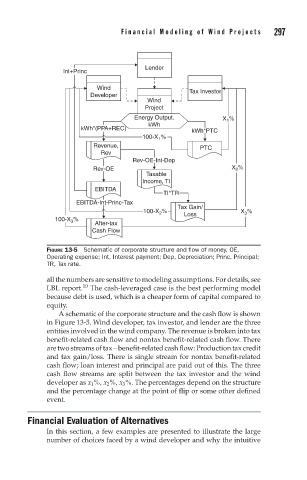

FIGURE 13-5 Schematic of corporate structure and flow of money. OE,

Operating expense; Int, Interest payment; Dep, Depreciation; Princ, Principal;

TR, Tax rate.

all the numbers are sensitive to modeling assumptions. For details, see

LBL report. 10 The cash-leveraged case is the best performing model

because debt is used, which is a cheaper form of capital compared to

equity.

A schematic of the corporate structure and the cash flow is shown

in Figure 13-5. Wind developer, tax investor, and lender are the three

entities involved in the wind company. The revenue is broken into tax

benefit-related cash flow and nontax benefit-related cash flow. There

are two streams of tax – benefit-related cash flow: Production tax credit

and tax gain/loss. There is single stream for nontax benefit-related

cash flow; loan interest and principal are paid out of this. The three

cash flow streams are split between the tax investor and the wind

developer as x 1 %, x 2 %, x 3 %. The percentages depend on the structure

and the percentage change at the point of flip or some other defined

event.

Financial Evaluation of Alternatives

In this section, a few examples are presented to illustrate the large

number of choices faced by a wind developer and why the intuitive