Page 552 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 552

538 The Complete Guide to Executive Compensation

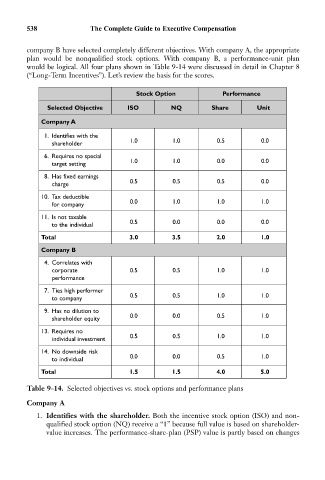

company B have selected completely different objectives. With company A, the appropriate

plan would be nonqualified stock options. With company B, a performance-unit plan

would be logical. All four plans shown in Table 9-14 were discussed in detail in Chapter 8

(“Long-Term Incentives”). Let’s review the basis for the scores.

Stock Option Performance

Selected Objective ISO NQ Share Unit

Company A

1. Identifies with the

1.0 1.0 0.5 0.0

shareholder

6. Requires no special

1.0 1.0 0.0 0.0

target setting

8. Has fixed earnings

0.5 0.5 0.5 0.0

charge

10. Tax deductible

0.0 1.0 1.0 1.0

for company

11. Is not taxable

0.5 0.0 0.0 0.0

to the individual

Total 3.0 3.5 2.0 1.0

Company B

4. Correlates with

corporate 0.5 0.5 1.0 1.0

performance

7. Ties high performer

0.5 0.5 1.0 1.0

to company

9. Has no dilution to

0.0 0.0 0.5 1.0

shareholder equity

13. Requires no

0.5 0.5 1.0 1.0

individual investment

14. No downside risk

0.0 0.0 0.5 1.0

to individual

Total 1.5 1.5 4.0 5.0

Table 9-14. Selected objectives vs. stock options and performance plans

Company A

1. Identifies with the shareholder. Both the incentive stock option (ISO) and non-

qualified stock option (NQ) receive a “1” because full value is based on shareholder-

value increases. The performance-share-plan (PSP) value is partly based on changes