Page 225 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 225

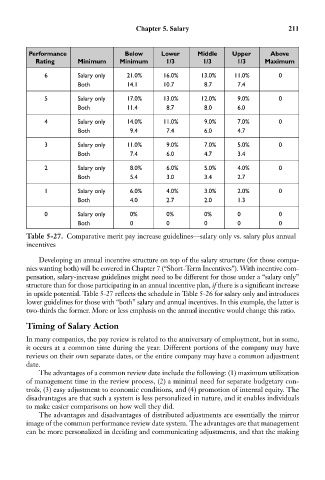

Chapter 5. Salary 211

Performance Below Lower Middle Upper Above

Rating Minimum Minimum 1/3 1/3 1/3 Maximum

6 Salary only 21.0% 16.0% 13.0% 11.0% 0

Both 14.1 10.7 8.7 7.4

5 Salary only 17.0% 13.0% 12.0% 9.0% 0

Both 11.4 8.7 8.0 6.0

4 Salary only 14.0% 11.0% 9.0% 7.0% 0

Both 9.4 7.4 6.0 4.7

3 Salary only 11.0% 9.0% 7.0% 5.0% 0

Both 7.4 6.0 4.7 3.4

2 Salary only 8.0% 6.0% 5.0% 4.0% 0

Both 5.4 3.0 3.4 2.7

1 Salary only 6.0% 4.0% 3.0% 2.0% 0

Both 4.0 2.7 2.0 1.3

0 Salary only 0% 0% 0% 0 0

Both 0 0 0 0 0

Table 5-27. Comparative merit pay increase guidelines—salary only vs. salary plus annual

incentives

Developing an annual incentive structure on top of the salary structure (for those compa-

nies wanting both) will be covered in Chapter 7 (“Short-Term Incentives”). With incentive com-

pensation, salary-increase guidelines might need to be different for those under a “salary only”

structure than for those participating in an annual incentive plan, if there is a significant increase

in upside potential. Table 5-27 reflects the schedule in Table 5-26 for salary only and introduces

lower guidelines for those with “both” salary and annual incentives. In this example, the latter is

two-thirds the former. More or less emphasis on the annual incentive would change this ratio.

Timing of Salary Action

In many companies, the pay review is related to the anniversary of employment, but in some,

it occurs at a common time during the year. Different portions of the company may have

reviews on their own separate dates, or the entire company may have a common adjustment

date.

The advantages of a common review date include the following: (1) maximum utilization

of management time in the review process, (2) a minimal need for separate budgetary con-

trols, (3) easy adjustment to economic conditions, and (4) promotion of internal equity. The

disadvantages are that such a system is less personalized in nature, and it enables individuals

to make easier comparisons on how well they did.

The advantages and disadvantages of distributed adjustments are essentially the mirror

image of the common performance review date system. The advantages are that management

can be more personalized in deciding and communicating adjustments, and that the making