Page 406 - Bruce Ellig - The Complete Guide to Executive Compensation (2007)

P. 406

392 The Complete Guide to Executive Compensation

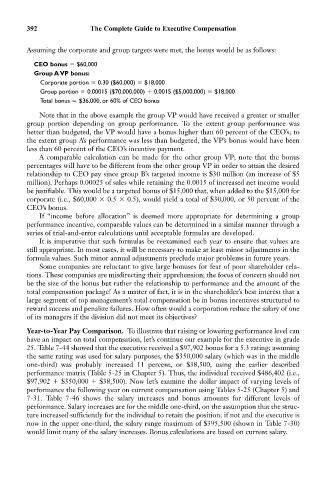

Assuming the corporate and group targets were met, the bonus would be as follows:

CEO bonus $60,000

Group A VP bonus:

Corporate portion 0.30 ($60,000) $18,000

Group portion 0.00015 ($70,000,000) 0.0015 ($5,000,000) $18,000

Total bonus $36,000, or 60% of CEO bonus

Note that in the above example the group VP would have received a greater or smaller

group portion depending on group performance. To the extent group performance was

better than budgeted, the VP would have a bonus higher than 60 percent of the CEO’s; to

the extent group A’s performance was less than budgeted, the VP’s bonus would have been

less than 60 percent of the CEO’s incentive payment.

A comparable calculation can be made for the other group VP; note that the bonus

percentages will have to be different from the other group VP in order to attain the desired

relationship to CEO pay since group B’s targeted income is $30 million (an increase of $5

million). Perhaps 0.00025 of sales while retaining the 0.0015 of increased net income would

be justifiable. This would be a targeted bonus of $15,000 that, when added to the $15,000 for

corporate (i.e., $60,000 0.5 0.5), would yield a total of $30,000, or 50 percent of the

CEO’s bonus.

If “income before allocation” is deemed more appropriate for determining a group

performance incentive, comparable values can be determined in a similar manner through a

series of trial-and-error calculations until acceptable formulas are developed.

It is imperative that such formulas be reexamined each year to ensure that values are

still appropriate. In most cases, it will be necessary to make at least minor adjustments in the

formula values. Such minor annual adjustments preclude major problems in future years.

Some companies are reluctant to give large bonuses for fear of poor shareholder rela-

tions. These companies are misdirecting their apprehension; the focus of concern should not

be the size of the bonus but rather the relationship to performance and the amount of the

total compensation package! As a matter of fact, it is in the shareholder’s best interest that a

large segment of top management’s total compensation be in bonus incentives structured to

reward success and penalize failures. How often would a corporation reduce the salary of one

of its managers if the division did not meet its objectives?

Year-to-Year Pay Comparison. To illustrate that raising or lowering performance level can

have an impact on total compensation, let’s continue our example for the executive in grade

25. Table 7-44 showed that the executive received a $97,902 bonus for a 5.3 rating; assuming

the same rating was used for salary purposes, the $350,000 salary (which was in the middle

one-third) was probably increased 11 percent, or $38,500, using the earlier described

performance matrix (Table 5-25 in Chapter 5). Thus, the individual received $486,402 (i.e.,

$97,902 $350,000 $38,500). Now let’s examine the dollar impact of varying levels of

performance the following year on current compensation using Tables 5-25 (Chapter 5) and

7-31. Table 7-46 shows the salary increases and bonus amounts for different levels of

performance. Salary increases are for the middle one-third, on the assumption that the struc-

ture increased sufficiently for the individual to retain the position; if not and the executive is

now in the upper one-third, the salary range maximum of $395,500 (shown in Table 7-30)

would limit many of the salary increases. Bonus calculations are based on current salary.