Page 134 - Applied Statistics Using SPSS, STATISTICA, MATLAB and R

P. 134

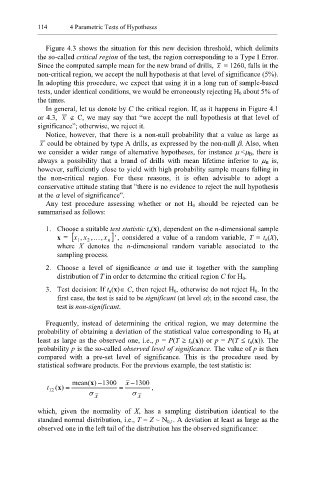

114 4 Parametric Tests of Hypotheses

Figure 4.3 shows the situation for this new decision threshold, which delimits

the so-called critical region of the test, the region corresponding to a Type I Error.

Since the computed sample mean for the new brand of drills, x = 1260, falls in the

non-critical region, we accept the null hypothesis at that level of significance (5%).

In adopting this procedure, we expect that using it in a long run of sample-based

tests, under identical conditions, we would be erroneously rejecting H 0 about 5% of

the times.

In general, let us denote by C the critical region. If, as it happens in Figure 4.1

or 4.3, x ∉ C, we may say that “we accept the null hypothesis at that level of

significance”; otherwise, we reject it.

Notice, however, that there is a non-null probability that a value as large as

x could be obtained by type A drills, as expressed by the non-null β. Also, when

we consider a wider range of alternative hypotheses, for instance µ <µ B, there is

always a possibility that a brand of drills with mean lifetime inferior to µ B is,

however, sufficiently close to yield with high probability sample means falling in

the non-critical region. For these reasons, it is often advisable to adopt a

“

conservative attitude stating that there is no evidence to reject the null hypothesis

at the α level of significance . ”

Any test procedure assessing whether or not H 0 should be rejected can be

summarised as follows:

1. Choose a suitable test statistic t n(x), dependent on the n-dimensional sample

’

x = [x , x ,K x , n ] , considered a value of a random variable, T ≡ t n(X),

2

1

where X denotes the n-dimensional random variable associated to the

sampling process.

2. Choose a level of significance α and use it together with the sampling

distribution of T in order to determine the critical region C for H 0.

3. Test decision: If t n(x)∈ C, then reject H 0, otherwise do not reject H 0. In the

first case, the test is said to be significant (at level α); in the second case, the

test is non-significant.

Frequently, instead of determining the critical region, we may determine the

probability of obtaining a deviation of the statistical value corresponding to H 0 at

least as large as the observed one, i.e., p = P(T ≥ t n(x)) or p = P(T ≤ t n(x)). The

probability p is the so-called observed level of significance. The value of p is then

compared with a pre-set level of significance. This is the procedure used by

statistical software products. For the previous example, the test statistic is:

−

mean (x ) − 1300 x 1300

t (x ) = = ,

12

σ X σ X

which, given the normality of X, has a sampling distribution identical to the

standard normal distribution, i.e., T = Z ~ N 0,1. A deviation at least as large as the

observed one in the left tail of the distribution has the observed significance: